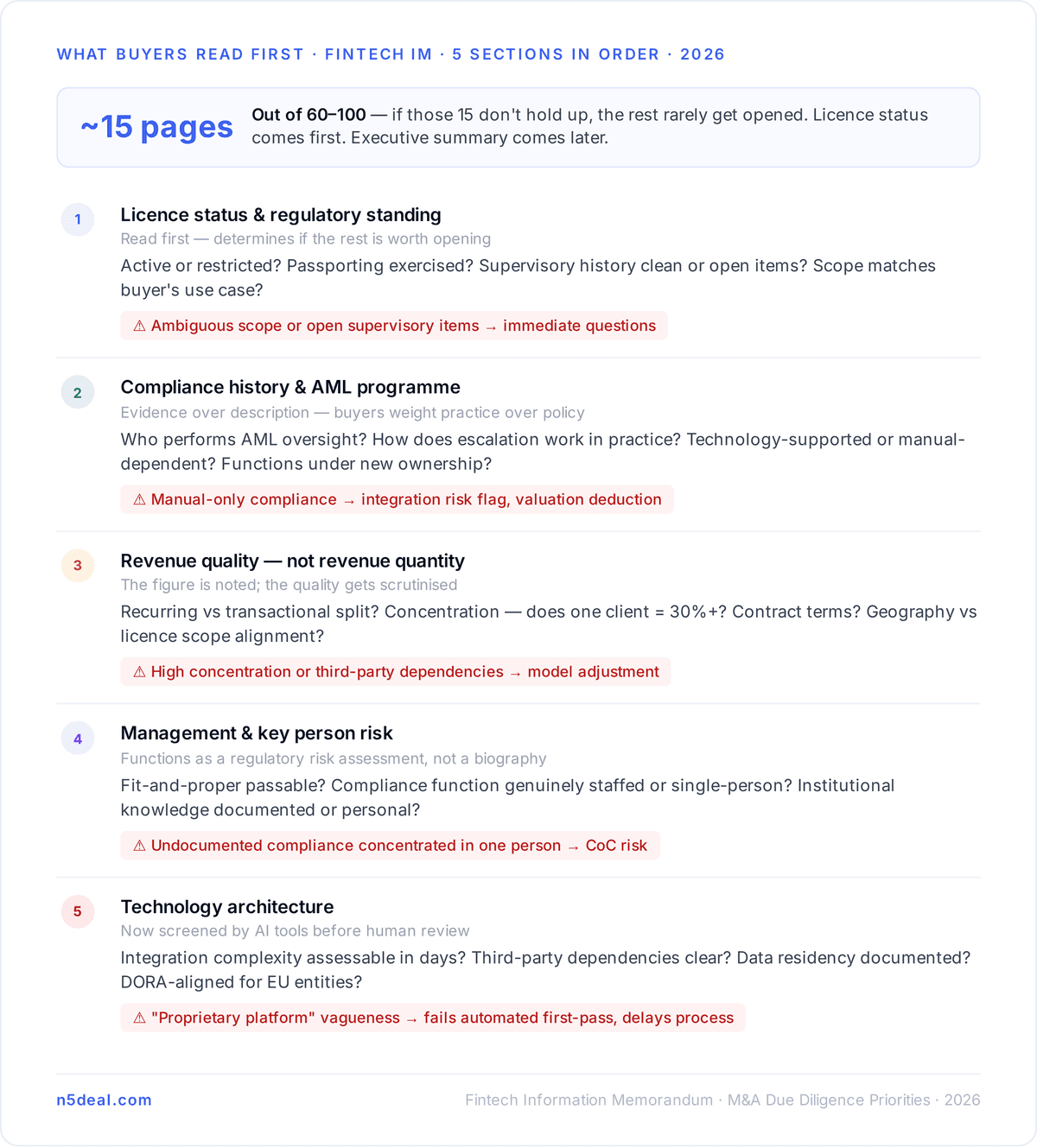

A fintech information memorandum typically runs 60 to 100 pages. A serious buyer reads roughly 15 of them first — and if those 15 pages don't hold up, the rest rarely get opened. Understanding which sections get read, in which order, and what buyers are actually looking for in each of them is the most practical preparation a founder can do before going to market. The gap between what sellers write and what buyers prioritise explains most of the late-stage repricing and deal collapse that fintech M&A practitioners see repeatedly.

Key Takeaways

Buyers of regulated fintech assets open the fintech information memorandum at the licence and regulatory status section — not the executive summary

Revenue quality and compliance history receive more scrutiny than revenue size — a clean AML programme with €5m revenue is more attractive to many buyers than a messy one with €20m

Acquirers in 2026 pay premiums for "plug-and-play" assets with regulatory compliance posture fully documented — incomplete compliance programmes are treated as valuation deductions, not negotiating points

Technology architecture sections are increasingly screened by automated tools before a human reviewer even opens the document

The management section functions as a regulatory risk assessment in licensed fintech deals — not a biography section

Section 1: Licence Status and Regulatory Standing

This is the section buyers read first, regardless of where it appears in the document. For a regulated fintech — EMI, PI, crypto-licensed, or banking-licensed — the authorisation is the primary asset. Its current status, scope, jurisdiction, and condition determine whether the rest of the IM is worth reading.

Buyers want to know: is the licence active, restricted, or under any supervisory attention? What activity types are explicitly covered? Does the authorisation include passporting rights, and have those rights been exercised? What is the relationship history with the supervising authority — routine correspondence, or remediation requirements?

Your regulatory posture matters more than many founders realise, especially in Europe or for assets handling cross-border flows. Being fully compliant with incoming regulations like PSD3 or MiCA can be a major value driver — it makes the asset a plug-and-play acquisition for buyers who want immediate market access without spending months resolving compliance issues post-close. A licence section that answers all of these questions cleanly, without requiring a buyer to ask follow-up questions, moves the process forward. One that leaves ambiguity creates due diligence requests before the formal process has begun.

Section 2: Compliance History and AML Programme

The second section buyers examine in detail is the compliance narrative — not the policy description, but the evidence of how the programme has actually functioned. There is a consistent gap between what an IM describes and what a compliance review discovers, and experienced buyers have learned to weight the evidence over the description.

Regulators expect robust oversight of third-party relationships — cloud providers, payment processors, KYC vendors. A vendor's failure becomes the licensee's compliance failure. Pre-onboarding due diligence, contract terms, and ongoing monitoring documentation are all reviewed during M&A due diligence.

Buyers want to see: who performed AML oversight, what the escalation path for suspicious activity looks like in practice, how KYC procedures were applied consistently across the customer base, and whether the compliance infrastructure would function under new ownership without a rebuild. Cloud-based AML solutions reached 69% adoption in 2025 — buyers now expect the compliance programme to be technology-supported, not manual-dependent, because manual programmes don't scale and don't survive ownership transitions cleanly.

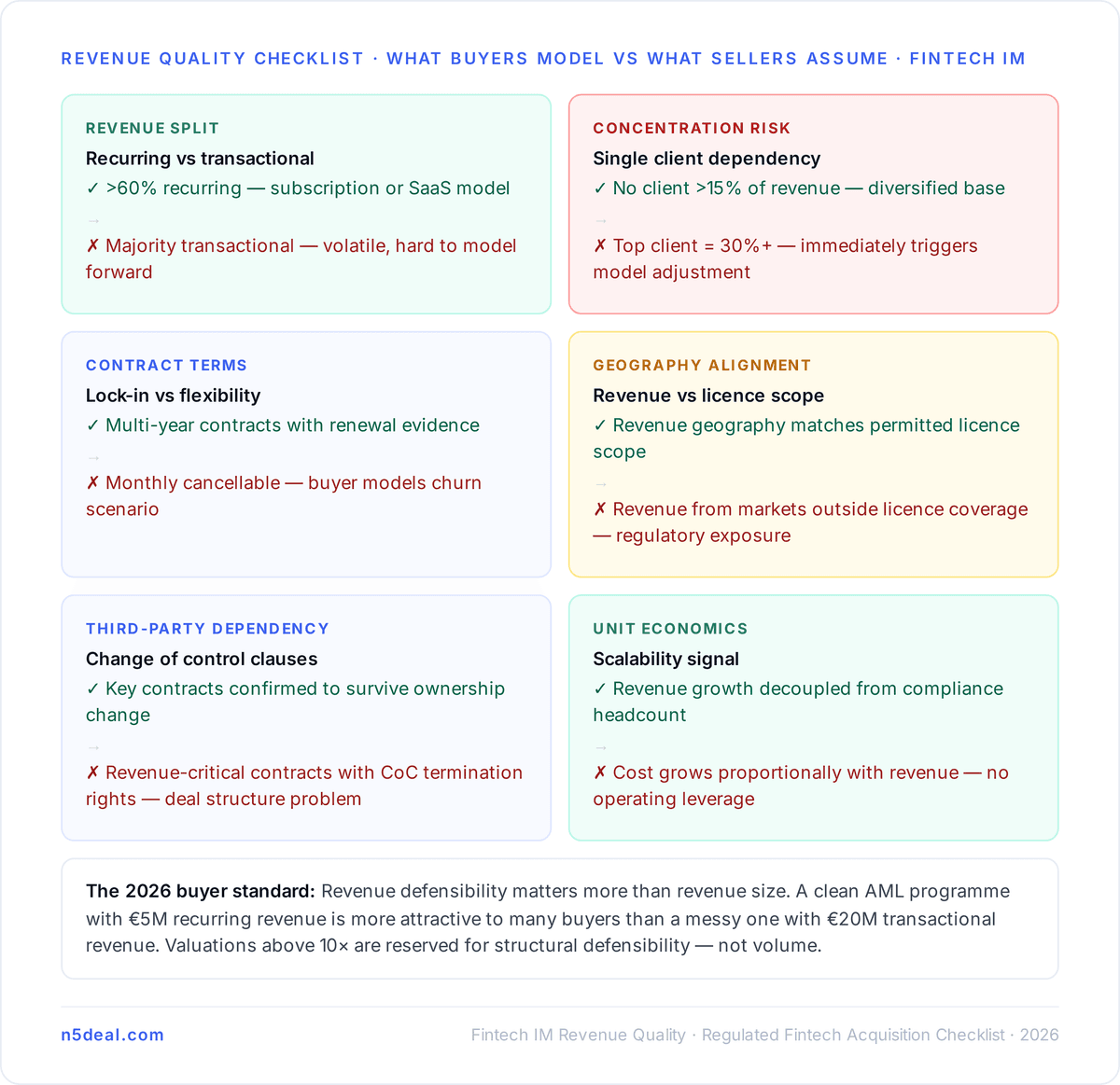

Section 3: Revenue Quality — Not Revenue Quantity

The revenue figure appears on the executive summary. Buyers note it and move on. What receives extended analysis is the revenue quality section — because in regulated fintech, revenue quality determines how a buyer models the asset post-acquisition.

The specific questions buyers are answering: what percentage of revenue is recurring versus transactional? What is customer concentration — does one enterprise client represent 30%+ of revenue? How do contract terms look — monthly cancellable versus multi-year? Does revenue geography align with the licence's permitted scope? Are there revenue streams that depend on third-party arrangements that may not survive a change of control?

In 2026, acquirers focus on profitable or close-to-profitable fintechs generating between £50m and £100m in annual revenues, with an uncompromising focus on unit economics, profitability, and scalable tech differentiation. Valuations above 10x revenue are reserved for companies demonstrating defensibility through structural advantages — data moats, AI-native operations, and regulatory compliance. Revenue size matters, but revenue defensibility matters more.

Section 4: Management and Key Person Risk

In regulated fintech, the management section of an IM functions as a regulatory risk assessment rather than a biographical summary. Buyers are evaluating: will key individuals pass fit-and-proper assessments during the change of control process? Is the compliance function genuinely staffed, or concentrated in one person? Are there founder dependencies that don't survive ownership transition?

The EU AI Act, adopted in April 2025, classifies credit-scoring models as high-risk systems, requiring digital lenders to publish detailed model cards outlining data inputs, test results, and fairness controls before licence renewal — solid AI governance and transparency are emerging as standard best practices that buyers now assess during diligence.

Beyond AI governance, buyers are assessing whether the management team has operated the compliance programme in a way that can be audited and replicated. A team that knows what the regulator expects and has documented evidence of meeting those expectations is a commercial asset. A team whose compliance record depends on undocumented institutional knowledge is an integration risk.

Section 5: Technology Architecture

AI tools can now ingest a 50-page memorandum and output a structured investment summary in seconds, flagging anomalies and generating deal-critical questions before deeper diligence begins. That means technology sections are now screened before a human reviewer applies judgement to them. An IM that describes technology in vague terms — "proprietary platform," "scalable infrastructure," "modern stack" — fails the automated first-pass review and generates questions that delay the process.

Buyers specifically want to know: is the architecture documented clearly enough that a technical team could assess integration complexity in days rather than weeks? What are the third-party dependencies? What data residency obligations apply? Does the technology pass operational resilience requirements under DORA for EU-regulated entities?

Conclusion

The fintech information memorandum sections that determine whether a deal proceeds are not the ones that receive the most writing effort. Licence status, compliance history, revenue quality, management risk, and technology architecture — in that order — are where experienced buyers concentrate their initial review. Sellers who front-load those five sections with specific, verifiable, well-organised information move through the process faster and with fewer late-stage surprises. Sellers who bury them in a narrative-heavy executive summary and a long company history section find that buyers arrive at due diligence with questions that a better-prepared document would have pre-empted. For sellers mapping what documentation a qualified buyer pool actually needs to see, N5Deal provides the market context and asset presentation structure that reflects what buyers in the current market are prioritising.

Disclaimer

This page is for informational purposes only. It does not constitute legal, financial, or regulatory advice. Readers should consult qualified professionals before making any decisions.

Frequently Asked Questions

Clear, concise info to help you understand the process!