A fintech data breach cost calculation that stops at the fine is missing most of the number. The average cost of a data breach in the financial sector reached $6.08 million in 2024 — a 10% year-on-year increase — and that figure covers direct incident costs only. For a licensed fintech, the full architecture of a breach cost includes regulatory penalties, licence consequences, counterparty relationship damage, customer attrition, and — if the company was approaching an exit — a material impact on deal valuation that can dwarf the direct costs. Most founders running compliance budgets against breach probability are working with numbers that undercount the actual exposure by a significant margin.

Key Takeaways

The average cost of a data breach in financial services is $6.08 million — but for a licensed fintech, the regulatory, reputational, and M&A consequences extend well beyond the direct incident cost

GDPR fines can reach €20 million or 4% of global annual turnover — by October 2025, cumulative GDPR fines had reached €6.7 billion, with the five largest 2025 fines alone exceeding €3 billion

DORA, effective January 2025, adds mandatory ICT incident reporting and resilience testing obligations that make breach consequences more visible to regulators and counterparties simultaneously

A data breach within 12 months of an M&A process can reduce valuation by 20–40% or trigger deal termination — the timing of a breach relative to an exit process is the most underestimated cost variable

35.5% of breaches in 2024 stemmed from third-party access — vendor risk management is now a standard due diligence item in both regulatory examinations and M&A processes

The Direct Cost Layer: Fines, Legal Fees, and Incident Response

The floor of a fintech data breach cost for an EU-regulated entity is set by GDPR. A GDPR breach can cost up to €20 million or 4% of annual global turnover, whichever is higher. Beyond fines, consequences include launch delays due to failed regulatory checks, reputational damage, and operational setbacks like forced service shutdowns or infrastructure overhauls.

The average GDPR fine is not the ceiling. The average fine was approximately €2.8 million in 2024, but penalties can reach €20 million or 4% of global turnover — with the highest fine to date exceeding €1 billion. For a licensed fintech operating across multiple EU jurisdictions, a breach that triggers notifications in several member states simultaneously multiplies both the regulatory exposure and the legal management cost.

Add incident response: forensic investigation, breach notification to affected individuals, regulatory correspondence, and technical remediation. For a company without a mature incident response plan, these costs compound quickly. Organisations using security AI and automation reduce average breach cost by up to $2.2 million compared to those without — the investment in prevention infrastructure has a measurable return when breach cost is correctly modelled.

The Regulatory Licence Layer: What Supervisors Do Next

For a licensed EMI, payment institution, or crypto-licensed entity, a data breach triggers a response that goes beyond the data protection authority. The prudential supervisor — the FCA, CBI, Bank of Lithuania, or equivalent — receives notification and assesses whether the breach indicates governance failures, inadequate operational resilience, or controls that don't meet licence conditions.

DORA, which came into force in January 2025, requires financial entities to implement ICT risk management, incident reporting, resilience testing, and third-party oversight. A major incident must be reported to the competent authority within specific timeframes — typically 4 hours for initial notification, 72 hours for an intermediate report. A breach that triggers a DORA major incident report creates a parallel regulatory process alongside the GDPR notification — two separate supervisory relationships managing responses to the same event, with different timelines, different requirements, and different consequences.

The outcome of that supervisory review can include remediation requirements, capital add-ons, restrictions on new business, or in serious cases, licence suspension. None of those outcomes appear in a direct breach cost calculation — but all of them are materially larger than the fine that preceded them.

The Commercial Layer: Counterparty, Customer, and Banking Partner Response

Licensed fintechs depend on banking relationships for safeguarding arrangements, payment scheme access, and correspondent services. Those relationships are contingent on regulatory standing, compliance posture, and operational credibility. A publicised breach damages all three simultaneously.

Trust is everything in financial services. A breach can lead to rapid customer churn and long-term reputational damage. Unlike other industries where customers may tolerate some level of risk, financial services customers move quickly when confidence is lost. Acquiring bank relationships — the contractual arrangements that allow a PSP or EMI to process transactions through card scheme infrastructure — include compliance audit rights and termination triggers for material regulatory events. A breach that results in a regulatory action can trigger those termination clauses before the fine is even calculated.

35.5% of breaches in 2024 stemmed from third-party access — which means the breach audit will examine every vendor relationship, API connection, and outsourced function. The remediation obligation extends beyond the fintech's own infrastructure to every third party that touched the affected data.

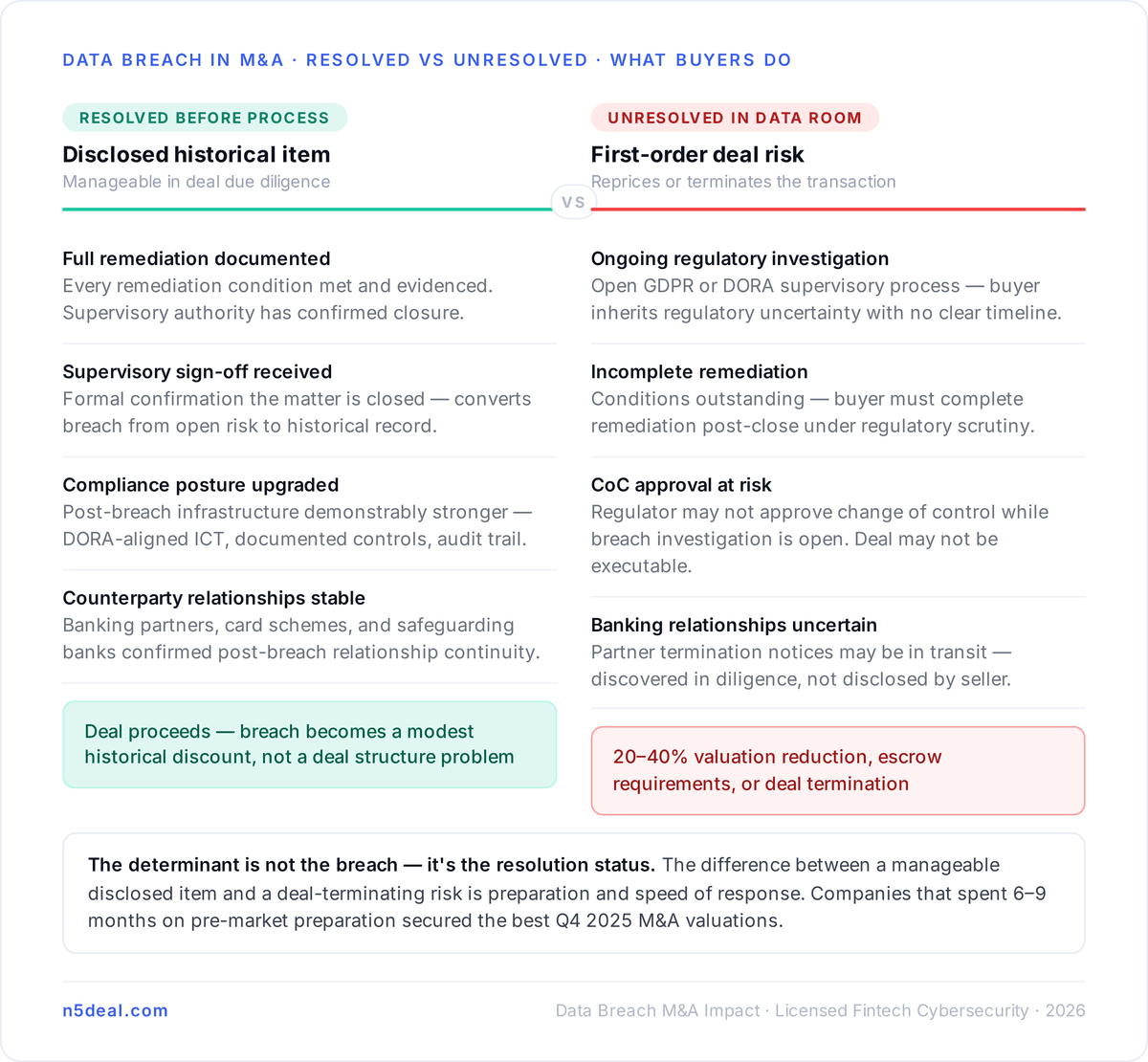

The M&A Layer: What a Breach Does to Exit Valuation

For a licensed fintech approaching an M&A exit, a data breach within 12 months of the process is one of the most consequential events that can occur. Buyers conducting diligence on a breached entity face a specific set of questions that extend the process and reduce the valuation: has the regulatory response been completed, is the remediation verified, are there outstanding enforcement matters, and does the compliance posture post-breach meet the standard required for a clean change of control approval?

A breach that is fully remediated, documented, and closed with the supervisory authority before a deal process begins is manageable — it becomes a disclosed historical item with a clear resolution. A breach that is ongoing, under investigation, or unresolved when a buyer opens the data room is a deal risk of the first order. The difference between those two outcomes is preparation and speed of response — not the breach itself.

Companies that secured the best M&A valuations in Q4 2025 spent 6 to 9 months on comprehensive diligence preparation before going to market, including technology and cybersecurity infrastructure assessment. The investment in that preparation is directly recoverable in deal terms. The cost of a breach that surfaces in due diligence is not.

Conclusion

The real fintech data breach cost for a licensed entity runs through four layers simultaneously: direct incident costs averaging $6 million in financial services, GDPR fines that can reach 4% of global turnover, regulatory licence consequences that supervisors impose independently of the data protection fine, and M&A valuation impact that can be multiples of both. The founders who manage breach risk most effectively are those who model the full cost architecture before an incident rather than after it — and who maintain the cyber and compliance infrastructure that reduces both breach probability and response cost when an incident occurs. For buyers assessing licensed fintech assets, cyber posture is a standard due diligence item that affects deal structure and price. For sellers, it's a preparation item that determines which buyers remain in the process. The licensed business marketplace at N5Deal presents assets with compliance documentation that allows buyers to assess this dimension before formal diligence begins.

Disclaimer

This page is for informational purposes only. It does not constitute legal, financial, or regulatory advice. Readers should consult qualified professionals before making any decisions.

Frequently Asked Questions

Clear, concise info to help you understand the process!