Hong Kong vs Singapore: Which Asian Hub Wins for Fintech M&A in 2026

The Hong Kong Singapore fintech M&A question doesn't have a universal answer — and anyone who gives you one without asking what kind of fintech you're building is probably not the right advisor. In 2026, both hubs have made significant regulatory advances, both have deepened their licensed asset ecosystems, and both are attracting serious institutional M&A interest. The difference is directional: Singapore is winning on payments infrastructure and Southeast Asian distribution, Hong Kong is winning on digital assets and Greater Bay Area access. Which one is worth more in a deal depends entirely on the buyer's commercial thesis.

Key Takeaways

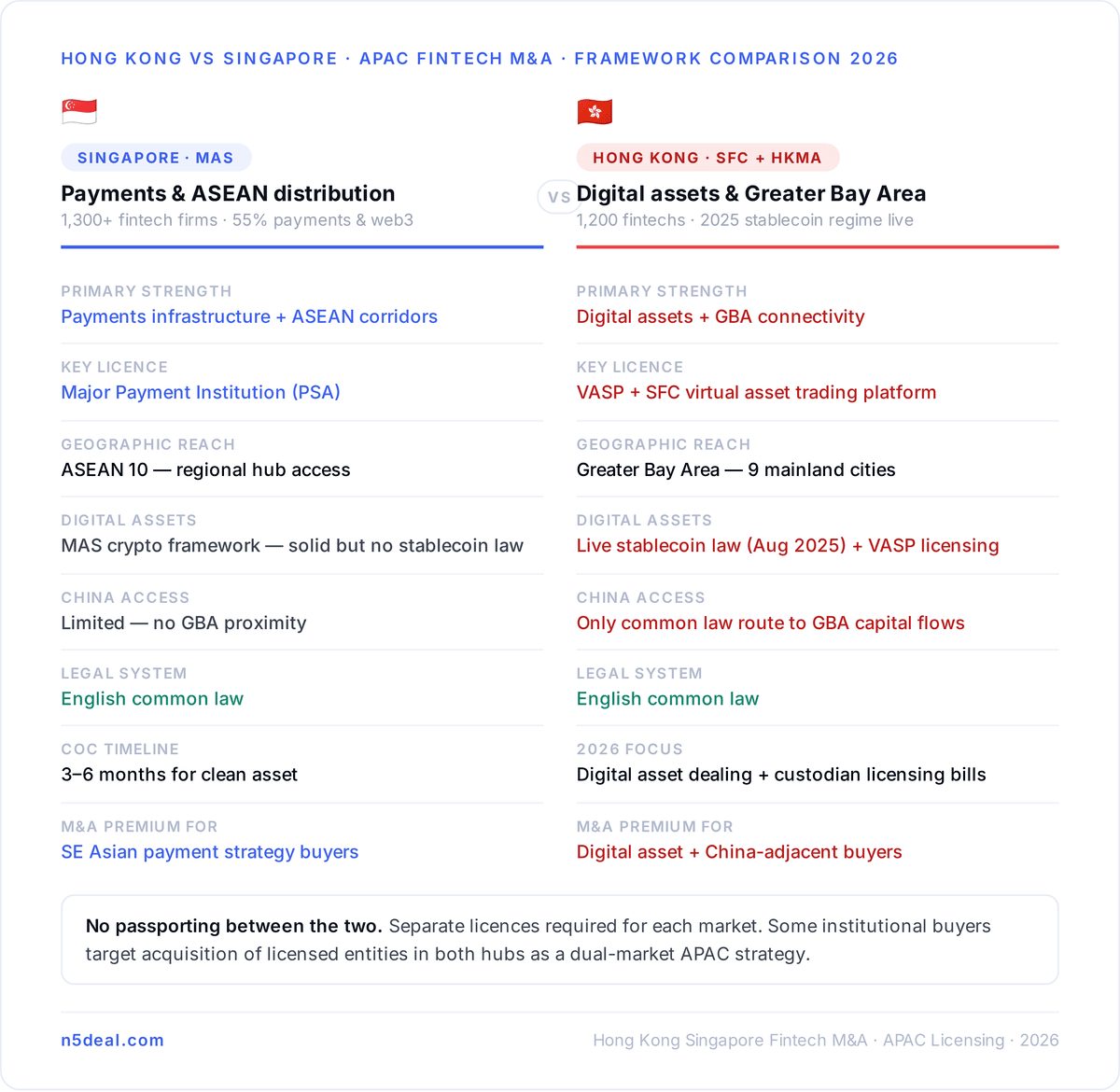

Hong Kong Singapore fintech M&A comparisons must start with asset type — the two hubs have diverged structurally, not just stylistically

Singapore's fintech sector has over 1,300 firms navigating MAS's multi-licence framework — approximately 55% concentrated in payments, web3, and regtech as of late 2024

Hong Kong has around 1,200 fintech companies in 2025, with the 2026-27 Budget publishing a second policy statement on digital assets and introducing bills for digital asset dealing and custodian service licensing

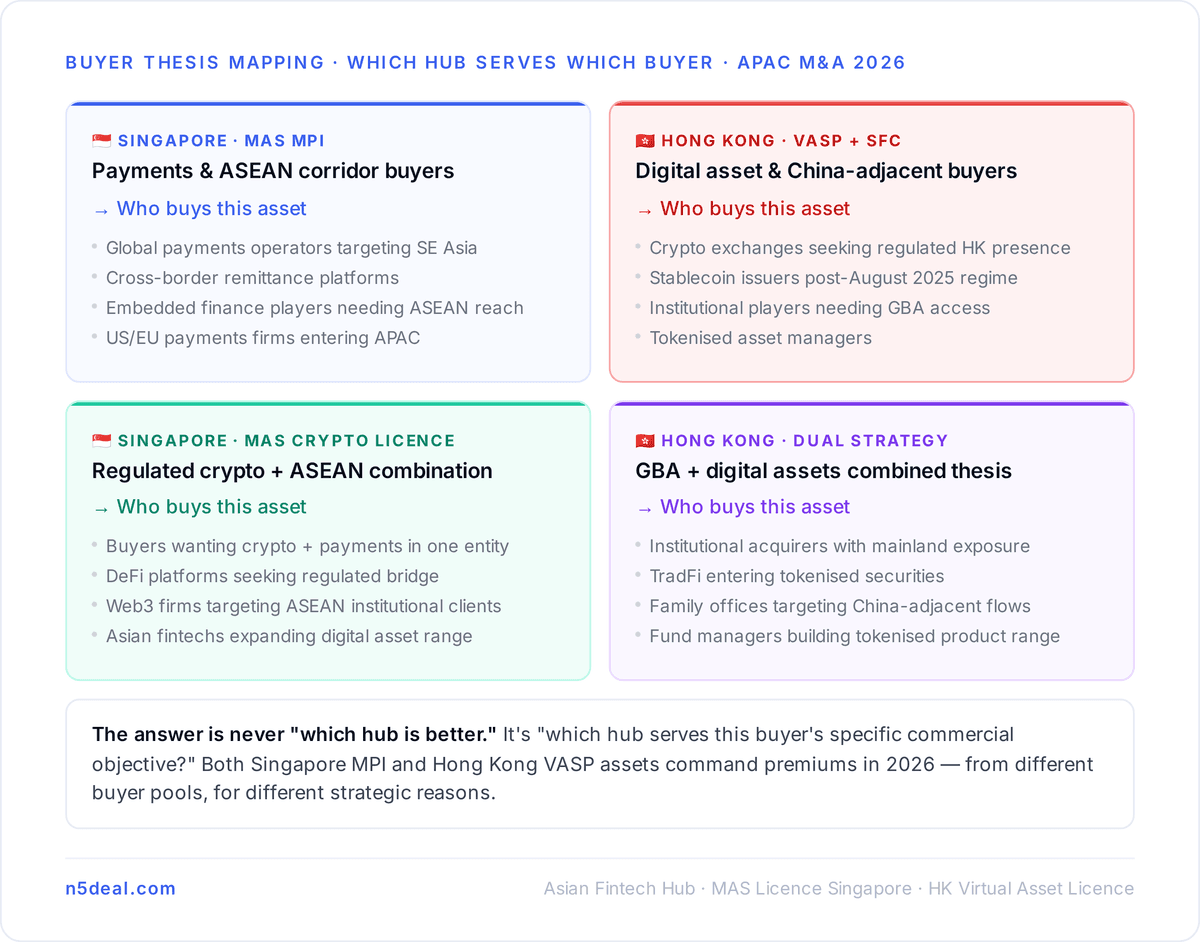

MAS licence Singapore assets command premiums from buyers targeting Southeast Asian corridors — the Major Payment Institution framework provides one of the most institutionally credible payment licences in APAC

Hong Kong's stablecoin regime came into effect August 1 2025, and its VASP licensing framework positions it as the only major financial centre with comprehensive virtual asset regulatory coverage — giving it a specific premium in crypto-adjacent M&A

Singapore: The Payments and Southeast Asia Play

Singapore's dominance in APAC fintech M&A for payment assets is structural. Singapore continues to lead as one of the world's most advanced fintech hubs, operating under MAS oversight with specialised licences including the Payment Services Act for digital payments, the Securities and Futures Act for capital markets, and the Financial Advisers Act for robo-advisors. That multi-licence framework is what makes Singapore valuable — not because it's simple, but because it's credible.

The MAS licence Singapore framework gives acquiring entities something specific: access to the ASEAN payment infrastructure and cross-border corridors that flow through Singapore as the region's financial hub. A Major Payment Institution licence under the PSA covers cross-border money transfer, domestic money transfer, and account issuance — the full stack for a payments operator targeting Southeast Asia. Buyers targeting the ASEAN corridor find Singapore the natural entry point — the MAS framework is institutionally trusted and the city-state's position as the region's financial hub provides distribution access that other jurisdictions can't replicate.

For M&A buyers, a Singapore MPI-licensed entity represents the fastest route to compliant payment operations across ASEAN. New licence applications take 6 to 12 months under MAS review. Acquiring an existing licensed entity compresses that to a change-of-control process, which for a clean asset can close in 3 to 6 months.

Hong Kong: The Digital Assets and GBA Play

Hong Kong's competitive advantage in 2026 is specific and significant. Hong Kong has consolidated its position as a leading global fintech hub through regulatory innovation, digital asset licensing, sovereign tokenisation, and cross-border financial connectivity with the Greater Bay Area. The 2026-27 Budget published a second policy statement on digital assets, with a bill introduced to establish licensing regimes for digital asset dealing and custodian service providers — expanding regulatory coverage beyond trading platforms.

The stablecoin regime that came into effect August 1 2025 positions Hong Kong as one of the few jurisdictions globally with a live, operational framework for stablecoin issuers. The SFC issued guidance enabling licensed virtual asset trading platforms in Hong Kong to link order books with affiliated overseas entities — widening liquidity access, expanding serviceable markets, and giving tokenised securities a stronger institutional footing.

For buyers whose thesis involves digital assets, tokenised securities, or cross-border connectivity with mainland China through the Greater Bay Area, Hong Kong has a specific and currently unmatched combination of regulatory frameworks. Singapore's MAS has a crypto licensing regime, but it does not have Hong Kong's proximity to mainland capital flows, its stablecoin-specific legislation, or its institutional infrastructure for tokenised asset issuance.

The Greater Bay Area Factor

Hong Kong's single most underrated M&A advantage in 2026 is not its regulatory framework — it's its position within the Greater Bay Area, the economic cluster encompassing Hong Kong, Macau, and nine mainland Chinese cities including Shenzhen and Guangzhou. The GBA has a combined GDP comparable to a mid-sized European economy and payment flows that dwarf any ASEAN corridor.

For a buyer whose commercial strategy includes mainland China access, a Hong Kong-licensed entity is the only route through a fully rule-of-law jurisdiction with common law courts, capital mobility, and an internationally recognised financial regulatory framework. Singapore offers no equivalent to that access. This factor rarely appears in comparative licensing analyses but is often the decisive consideration in institutional M&A targeting APAC.

What the 2026 Data Shows

Both hubs are generating active deal flow. Asian institutions operating across Singapore, Hong Kong, Japan and Dubai are differentiating themselves on regulatory competence and transparent risk management — which means that well-regulated licensed assets in both hubs are receiving premium valuations relative to unlicensed equivalents.

The pattern is consistent with what N5Deal observes in APAC-focused mandates: buyers with Southeast Asian payment strategies target Singapore MPI assets; buyers with digital asset or China-adjacent theses target Hong Kong VASP and SFC-licensed entities. Both categories are active. Both are commanding premiums over unlicensed structures. The question is never "which hub is better?" — it's "which hub serves this buyer's specific commercial objective?"

Conclusion

Hong Kong Singapore fintech M&A in 2026 is not a competition — it's a functional division of the APAC market. Singapore owns payments infrastructure and ASEAN distribution. Hong Kong owns digital assets, stablecoin regulation, and Greater Bay Area access. A licensed Singapore MPI or a licensed Hong Kong VASP both carry premiums in deal processes — because the buyers who need what each one provides are motivated and well-capitalised. For founders mapping APAC exit options and buyers evaluating licensed APAC assets, N5Deal catalogues licensed fintech entities across jurisdictions with the compliance documentation needed to assess regulatory standing before engaging formal processes.

Disclaimer

This page is for informational purposes only. It does not constitute legal, financial, or regulatory advice. Readers should consult qualified professionals before making any decisions.

Frequently Asked Questions

Clear, concise info to help you understand the process!