Discover proven strategies to grow your money transfer business in 2025. Learn how to scale, boost customer trust, and improve cross-border efficiency.

How to Grow Your Money Transfer Business in 2025

The global money transfer business is experiencing unprecedented transformation. With cross-border remittances projected to exceed $930 billion by the end of 2025, operators who understand the mechanics of sustainable growth are capturing significant market share while others struggle with outdated infrastructure and compliance challenges.

If you're running a money transfer business or exploring how to start money transfer business operations, you're likely facing critical questions: How do you scale while maintaining regulatory compliance? Which technology investments deliver measurable returns? How do you compete against both fintech disruptors and established financial institutions?

This comprehensive guide examines what a money transfer business is, the market forces shaping 2025, and the strategic, technological, and marketing approaches that drive profitable growth. You'll discover regulatory requirements, customer acquisition strategies, and when to seek specialized guidance from financial and legal professionals.

Key Takeaways

Money transfer business fundamentals: A regulated financial service facilitating domestic and international fund transfers, generating revenue through transaction fees and foreign exchange spreads

2025 market dynamics: Emerging markets, mobile-first platforms, and real-time settlement infrastructure are driving double-digit growth in specific corridors

Strategic expansion priorities: Geographic diversification, product bundling, and local partnerships outperform generic scaling approaches

Technology as competitive advantage: API integrations, fraud prevention systems, and cloud infrastructure are essential for sustainable operations

Customer acquisition essentials: Digital marketing, referral programs, and community partnerships deliver highest ROI when tailored to corridor-specific demographics

Regulatory compliance value: Proactive AML and KYC processes build trust and unlock institutional partnerships that create competitive moats

What Is a Money Transfer Business?

A money transfer business is a regulated financial service provider that enables individuals and companies to send funds domestically or across international borders. The business acts as an intermediary between senders and recipients, facilitating transactions that might otherwise be impossible or prohibitively expensive through traditional banking channels.

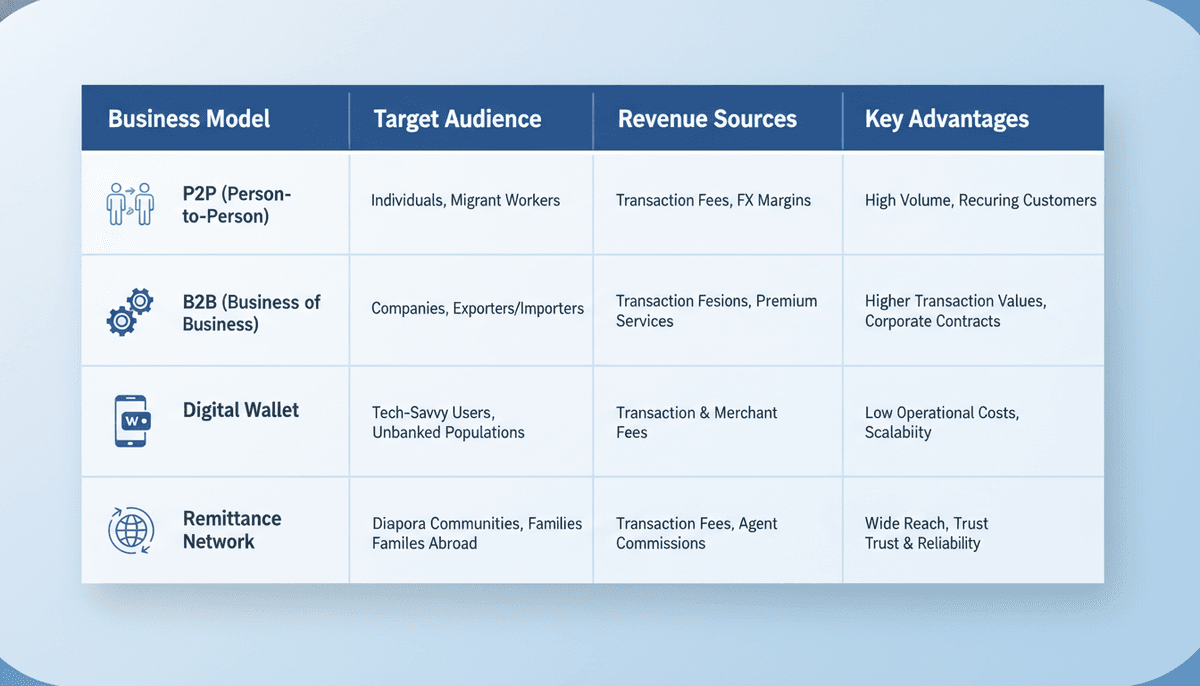

The industry operates through three distinct models:

Person-to-Person (P2P) transfers: Individual remittances to family members abroad, representing the largest segment by transaction volume and the primary revenue driver for most operators

Business-to-Business (B2B) transfers: Commercial payments including supplier settlements, international payroll, and cross-border trade transactions requiring higher transaction limits and specialized compliance

International money transfers: Cross-border transactions encompassing both P2P and B2B categories, involving currency conversion and multi-jurisdictional regulatory compliance

Money transfer businesses generate income through two primary channels. Transaction fees represent the explicit charge per transfer, typically structured as flat fees for smaller amounts or percentage-based fees for larger transactions. Foreign exchange spreads constitute the difference between interbank rates and customer rates, often accounting for 40-60% of total revenue in high-volume corridors.

When customers initiate transfers, the money transfer business collects funds through various channels: cash at agent locations, bank transfers, debit cards, or digital wallets. The operator then routes the transaction through correspondent banking networks, payment processors, or proprietary settlement systems. On the receiving end, funds are disbursed via bank deposit, mobile money accounts, cash pickup at agent locations, or home delivery in some markets.

Your money transfer business is only as reliable as your weakest link in this chain—which is why infrastructure investments matter more than marketing budgets in the early stages.

Market Trends & Growth Drivers in 2025

The money transfer business landscape in 2025 is shaped by three powerful forces: technological acceleration, shifting demographic patterns, and evolving regulatory frameworks. Understanding these trends directly impacts where you allocate capital and which markets you enter.

Explosive Growth in Emerging Corridors

While traditional corridors like US-to-Mexico or UK-to-India remain substantial, the fastest growth is happening in South-South corridors—transfers between emerging economies. Intra-African remittances grew 23% year-over-year in 2024, driven by mobile money adoption and regional payment integration initiatives. Southeast Asian corridors, particularly involving migrant workers in Gulf Cooperation Council countries, show similar momentum.

Data from the World Bank suggest that reducing transfer costs by just 5 percentage points in these corridors could unlock an additional $16 billion annually for recipient households. Regional demand is increasingly influenced by diaspora populations with higher digital literacy. Younger senders (ages 25–40) prefer mobile-first platforms with transparent pricing, while older demographics still value agent networks and cash options.

Technology-Driven Customer Expectations

Key technology trends reshaping the industry:

Real-time settlement has shifted from premium feature to baseline expectation, with customers comparing services to instant payment experiences like Venmo or Zelle

Mobile money transfers now account for over 35% of global remittance volume, up from 18% in 2020

Blockchain-enabled settlement networks and central bank digital currencies (CBDCs) are moving from pilot programs to production in several jurisdictions

Digital wallets have become the preferred payout method in markets like Kenya, the Philippines, and Bangladesh, where banking penetration lags but smartphone adoption exceeds 70%

If your platform doesn't integrate seamlessly with popular digital wallets in your target corridors, you're effectively invisible to a growing customer segment.

Regulatory Harmonization and Compliance Technology

Regulatory frameworks are slowly converging around common standards for anti-money laundering (AML) and know-your-customer (KYC) requirements, but implementation varies dramatically by jurisdiction. The Financial Action Task Force (FATF) continues to pressure countries to strengthen oversight, which means compliance costs are rising—but so is the competitive moat for operators who invest in robust systems.

Regulatory technology (RegTech) solutions now automate much of the compliance burden, using AI to flag suspicious transactions and streamline customer verification. Operators who treat compliance as a strategic advantage—rather than a cost center—are winning institutional partnerships and correspondent banking relationships that smaller players can't access.

Strategic Approaches for Expansion

Growing your money transfer business requires more than adding new corridors or increasing marketing spend. The operators who scale successfully in 2025 are those who think systematically about market entry, product evolution, and partnership strategy.

Geographic Expansion: Corridor Selection Framework

Not all corridors are created equal. Before entering a new market, evaluate four key factors:

Critical factors for corridor selection:

Volume and growth trajectory: Use World Bank remittance data as a baseline to identify high-potential markets

Regulatory complexity: Evaluate licensing requirements and compliance burden in both sending and receiving countries

Competitive intensity: Assess pricing dynamics and market saturation to identify opportunities

Operational capacity: Determine your ability to serve the corridor effectively with existing infrastructure

High-volume corridors like US-to-Mexico are attractive but intensely competitive, with razor-thin margins. Emerging corridors may offer higher margins but require significant customer education and agent network development. A practical approach is to identify corridors where you have a structural advantage—perhaps existing relationships with banks in the destination country, or deep cultural knowledge of the diaspora community you're serving.

Consider a tiered expansion strategy. Start with one or two corridors where you can achieve operational excellence and strong unit economics. Once you've refined your processes and built a repeatable playbook, expand to adjacent corridors that share similar characteristics. This disciplined approach outperforms the "spray and pray" method of launching in dozens of corridors simultaneously.

Product Diversification and Bundling

The most successful money transfer businesses in 2025 don't just move money—they solve adjacent financial needs for their customers. Bill payment services allow senders to pay utilities, school fees, or loan installments directly on behalf of recipients, creating stickiness and increasing transaction frequency. Micro-insurance products add revenue with minimal operational overhead. Savings and investment products, offered in partnership with licensed financial institutions, help you capture more wallet share from customers who trust your brand.

Product bundling works particularly well when tailored to specific use cases. A "family support package" might combine regular remittances with bill payment and mobile airtime top-up. A "business corridor bundle" could include B2B transfers, FX hedging tools, and trade finance referrals. The key is to start with your customers' actual needs and build products that solve real problems.

Strategic Partnerships and White-Label Opportunities

Partnerships can accelerate growth faster than organic expansion, but they require careful structuring. Agent network partnerships with retail chains, post offices, or microfinance institutions extend your physical footprint without the capital expense of owned locations. Technology partnerships with core banking providers, payment processors, or identity verification services let you leverage best-in-class infrastructure without building it yourself.

White-label opportunities—where you provide the underlying money transfer infrastructure for another brand—can be highly profitable if you have excess capacity and strong unit economics. Banks, retailers, and telecom operators often want to offer remittance services to their customers but lack the regulatory licenses and operational expertise.

One caution: partnerships introduce dependencies and potential conflicts of interest. Always structure agreements with clear performance metrics, exit clauses, and intellectual property protections. Consult with an attorney experienced in financial services partnerships before signing any significant deal.

Technology & Infrastructure Enhancements

Technology is no longer a differentiator in the money transfer business—it's the price of entry. But the specific technology choices you make will determine whether you scale profitably or burn cash fighting technical debt.

Platform Architecture and Scalability

Your core transfer platform must handle three critical functions: transaction processing and routing, compliance screening and reporting, and customer management and support. Many operators make the mistake of building custom solutions for everything, which creates maintenance nightmares and slows feature development.

A more pragmatic approach is to use a modular architecture. License or build a robust core transaction engine that handles the critical path. Integrate best-of-breed third-party services for non-core functions like identity verification, fraud detection, customer communication, and analytics. This lets you move faster, reduce development costs, and swap components as better solutions emerge.

Cloud infrastructure is non-negotiable for scalability. Operators still running on-premise servers face capacity constraints during peak periods and struggle to expand into new regions quickly. Major cloud providers offer financial-services-grade security, compliance certifications, and global infrastructure that would cost millions to replicate.

API Integration and Ecosystem Connectivity

Your money transfer business doesn't exist in isolation—it's part of a broader financial ecosystem. API integrations determine how easily you can connect with banks, mobile money operators, payment networks, and other partners. Operators with well-documented, reliable APIs attract more partnerships and can launch new corridors faster.

Prioritize integrations that directly impact customer experience:

Real-time bank account verification reduces fraud and failed transactions

Direct integrations with mobile money platforms (M-Pesa, GCash, bKash) eliminate intermediary fees and speed up payouts

Connections to FX liquidity providers help you offer competitive rates while managing currency risk

One often-overlooked integration is with your own data warehouse and analytics platform. You should be able to answer questions like: What's my customer acquisition cost by channel and corridor? Which customer segments have the highest lifetime value? Where are transactions failing, and why?

Security, Fraud Prevention, and Transaction Monitoring

Fraud is the silent killer of money transfer businesses. A single major fraud incident can wipe out months of profit and trigger regulatory scrutiny that damages your reputation and operating licenses. Your security posture must be proactive, not reactive.

Multi-layered fraud detection combines rule-based systems with machine learning models that identify anomalous patterns. Behavioral biometrics analyze how customers interact with your platform—typing speed, mouse movements, device fingerprints—to detect account takeovers. Real-time transaction monitoring screens against sanctions lists, politically exposed persons (PEP) databases, and adverse media.

Invest in a dedicated fraud operations team, even if it's just one or two people initially. They should review flagged transactions, investigate suspicious patterns, and continuously tune your detection systems. The cost of this team is a fraction of what you'll lose to fraud—or pay in regulatory fines—if you neglect this function.

Marketing & Customer Acquisition Tactics

You can build the best money transfer platform in the world, but if customers don't know about it—or don't trust it—you won't grow. Effective customer acquisition in 2025 requires a mix of digital marketing, community engagement, and strategic incentives.

Digital Marketing and Corridor-Specific Targeting

Generic "send money abroad" campaigns rarely work. The most effective marketing speaks directly to specific diaspora communities, in their language, addressing their unique concerns. A campaign targeting Filipino nurses in the US sending money home will look completely different from one targeting Nigerian students in the UK.

Search engine marketing (SEM) remains highly effective for high-intent keywords like "send money to [country]" or "cheapest way to transfer money to [city]." Focus on long-tail keywords with lower competition and higher conversion intent. Your landing pages should be corridor-specific, showing exact fees and exchange rates for that route, customer testimonials from that community, and payout options relevant to that destination.

Social media marketing works best when it's community-driven rather than promotional. Sponsor local cultural events, partner with diaspora influencers, and create content that provides genuine value. Facebook and WhatsApp remain dominant channels for many diaspora communities, while younger segments increasingly discover services through TikTok and Instagram.

Referral Programs and Incentive Structures

Your existing customers are your best acquisition channel—if you give them a reason to spread the word. Referral programs work particularly well in the money transfer business because trust is paramount, and personal recommendations carry enormous weight.

Structure your referral program to reward both the referrer and the new customer. A typical model offers $10–25 in transfer credits to the referrer when their friend completes their first transaction, and a discount or fee waiver for the new customer. Make the referral process frictionless: unique referral links, in-app sharing to WhatsApp or SMS, and automatic credit application without requiring codes or forms.

Track referral program economics carefully. Calculate the customer acquisition cost (CAC) for referred customers versus other channels, and the lifetime value (LTV) of referred customers. In most cases, referred customers have higher retention and LTV because they come pre-qualified through a trusted recommendation.

Community Partnerships and Agent Network Development

Physical presence still matters, especially for cash-based transactions and customers who prefer face-to-face service. Building an agent network—retail locations where customers can initiate transfers and recipients can collect cash—extends your reach without the overhead of owned branches.

Ideal agent partners include grocery stores, check-cashing outlets, mobile phone shops, and money service businesses in areas with high immigrant populations. Offer agents competitive commission structures (typically 1–3% of transaction value) and provide training, marketing materials, and technical support.

Community partnerships go beyond transactional agent relationships. Sponsor diaspora associations, cultural festivals, and community radio programs. Offer financial literacy workshops at community centers and places of worship. These investments build brand awareness and trust in a way that paid advertising cannot replicate.

Regulatory & Compliance Considerations

Regulatory compliance is expensive, complex, and absolutely non-negotiable. But operators who excel at compliance gain competitive advantages that more than offset the costs.

Licensing Requirements and Jurisdictional Complexity

In most jurisdictions, a money transfer business is a money services business (MSB) or payment institution that requires specific licenses to operate legally. Requirements vary dramatically by country and even by state or province within countries.

In the United States, you need to register with FinCEN (Financial Crimes Enforcement Network) at the federal level and obtain money transmitter licenses in each state where you operate—a process that can take 12–24 months and cost $500,000–2,000,000 depending on how many states you enter. The European Union offers a more streamlined path through the Payment Services Directive (PSD2), where a license in one member state can passport to others.

Before entering any new market, consult with a local attorney who specializes in financial services regulation—this is not an area where you can rely on Google research or generic advice.

AML, KYC, and Transaction Monitoring Obligations

Anti-money laundering (AML) and know-your-customer (KYC) requirements are the backbone of money transfer regulation. You must verify the identity of every customer, understand the source of their funds, and monitor transactions for suspicious activity. Failure to comply results in fines, license revocation, and potential criminal liability for executives.

KYC procedures typically require collecting and verifying government-issued identification, proof of address, and in some cases, source of funds documentation for large or frequent transactions. Modern identity verification services can automate much of this process, using document scanning, facial recognition, and database checks to verify identities in seconds rather than days.

Transaction monitoring systems must screen every transfer against sanctions lists (OFAC, UN, EU), PEP databases, and your own risk rules. Suspicious activity must be investigated and, if warranted, reported to authorities through Suspicious Activity Reports (SARs) or equivalent filings.

Building Compliance as a Competitive Advantage

Most operators treat compliance as a cost center and minimize investment. The smart operators recognize that robust compliance unlocks opportunities that non-compliant competitors can't access.

Banks and payment networks are increasingly selective about which money transfer businesses they'll work with. A strong compliance program—documented policies, trained staff, regular audits, and a clean regulatory record—makes you an attractive partner. This translates to better correspondent banking relationships, lower reserve requirements, and access to more efficient settlement networks.

Institutional customers (corporations, NGOs, government agencies) require their money transfer providers to meet high compliance standards. If you can demonstrate SOC 2 certification, regular third-party audits, and robust AML controls, you can win B2B contracts that generate high-volume, predictable revenue streams.

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, or business advice. The money transfer industry is heavily regulated, and requirements vary significantly by jurisdiction. Always consult with qualified professionals—including financial services attorneys, compliance consultants, and certified public accountants—for guidance specific to your business circumstances and target markets. Regulatory requirements change frequently; verify current requirements with appropriate authorities before making business decisions.

Frequently Asked Questions

Clear, concise info to help you understand the process!