US investors EU fintech opportunities are driven by scalability, regulatory clarity, and revenue quality. Transatlantic fintech investment is increasing, but with stricter diligence and clearer mandates. US buyers focus on infrastructure, payments, and regulated platforms in US fintech M&A Europe. Successful cross-border fintech deals require alignment on governance, reporting, and growth strategy. Understanding EU fintech investment mandates is essential for founders targeting US capital.

Why US Capital Is Looking at Europe Again

After a period of domestic focus, US interest in EU fintech is clearly returning in 2026. The reasons are structural. Europe offers regulatory frameworks that are increasingly predictable. Many EU fintechs are now more disciplined businesses, shaped by tighter funding conditions. And valuations remain relatively attractive compared to US peers.

This combination is driving a new wave of transatlantic fintech investment, but it is more selective than previous cycles. US investors are not simply expanding geographically — they are targeting specific profiles with clear thesis alignment.

What US Investors Are Actually Looking For

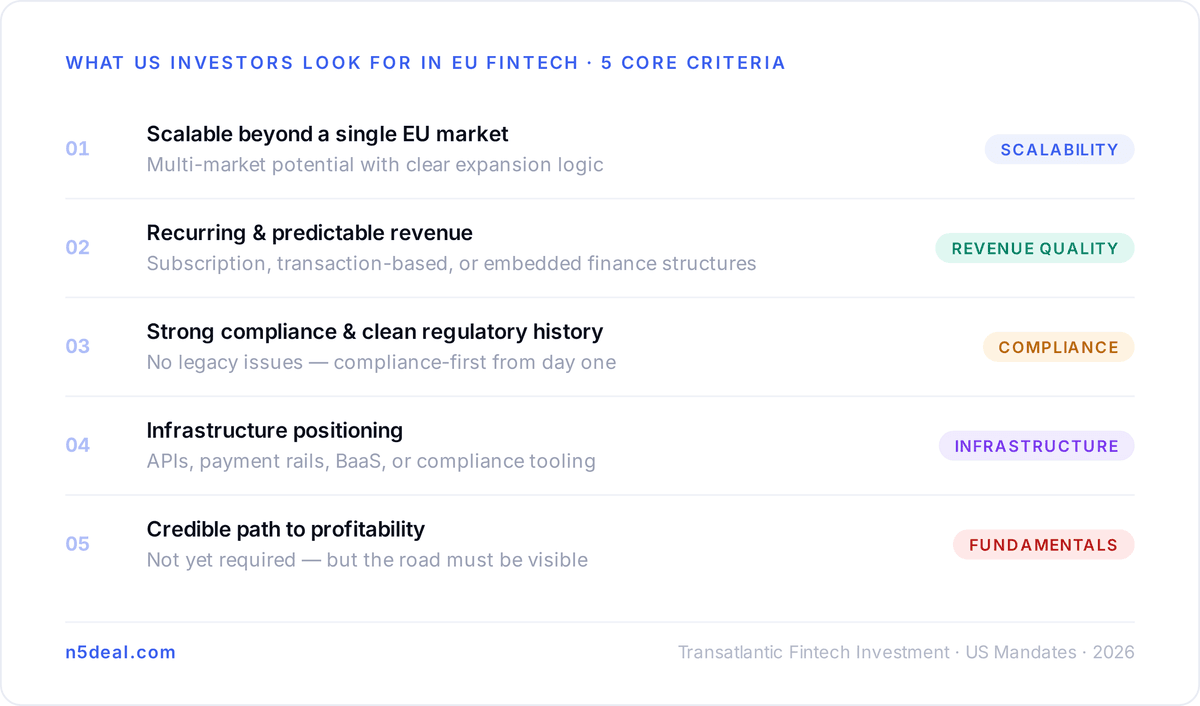

Understanding EU fintech investment mandates starts with recognizing that US capital is highly thesis-driven. Investors typically pursue assets that fit strategic priorities rather than opportunistic expansion. Across US investors EU fintech conversations, five criteria consistently surface: scalable business models that can expand beyond a single EU market, recurring and predictable revenue from subscription, transaction-based, or embedded finance structures, strong compliance frameworks with clean regulatory history, infrastructure positioning in APIs, payments rails, BaaS, or compliance tooling, and a credible path to profitability even if not yet achieved. These expectations reflect broader trends in US venture capital Europe, where capital efficiency and resilience now matter as much as growth velocity.

The Role of M&A in Transatlantic Strategy

Beyond minority investments, US fintech M&A Europe is becoming an important market entry strategy. For many US companies, acquiring a European platform is faster and lower-risk than building from scratch. Typical motivations include accessing EU licenses and regulatory permissions, entering new markets with an existing customer base, acquiring infrastructure or technical capabilities, and accelerating product expansion through integration. However, cross-border fintech deals are structurally complex. Differences in regulation, culture, and operating models require careful planning well before any term sheet is signed.

Key Differences in Expectations

One of the most significant challenges in transatlantic fintech investment is the expectation gap between US investors and EU founders. US investors typically expect faster decision-making and execution, more aggressive scaling strategies, standardized reporting and metrics, and stronger alignment on governance and board control. EU founders, on the other hand, often prioritize regulatory stability, sustainable growth over rapid expansion, and the preservation of local market expertise. Bridging this gap early — through shared frameworks and clear communication — is essential for partnerships that last beyond the initial close.

Where US Capital Is Flowing

Not all fintech sectors are equally attractive. Current US venture capital Europe activity shows strong interest in payments and payment infrastructure, embedded finance platforms, compliance and regtech solutions, data-driven lending and risk models, and BaaS and API-driven financial services. These sectors align with global scalability and integration potential, making them well-suited for both investment and US fintech M&A Europe strategies.

What Founders Should Do to Attract US Investors

For EU founders targeting US investors EU fintech capital, preparation and positioning are equally important. Aligning metrics and reporting with US investor expectations, demonstrating scalability beyond local markets, strengthening compliance and governance frameworks, clearly articulating a global expansion strategy, and engaging advisors experienced in cross-border transactions all increase the likelihood of productive conversations. How a company presents its growth story can influence investor perception as much as the underlying performance data.

Conclusion

The resurgence of US interest in EU fintech marks an important shift in global fintech dynamics. Europe is no longer treated as a secondary market — it is a strategic opportunity. But success in transatlantic fintech investment requires genuine alignment. Founders must understand US expectations, while investors must adapt to European regulatory and operational realities. For both sides, well-structured partnerships and acquisitions can unlock significant cross-border value.

Disclaimer:

This article is for informational purposes only and does not constitute legal, financial, or investment advice. Cross-border transactions involve regulatory, tax, and operational complexities. Readers should consult qualified professionals before making decisions.

Frequently Asked Questions

Clear, concise info to help you understand the process!